With Trump’s election win, world is fast moving from roaring 2020s theme to a very negative economic outlook over next few years. Troubles didn’t start with Trump but Trump administration is surely triggering the negative prospect. He is calling it “Make America Great Again” but now whole world is at a very different place than what it was before 2020. Asset markets are overstretched and income uncertainty has risen world over. The more the two diverge, the more significant the problem.

China’s problem has become world’s problem

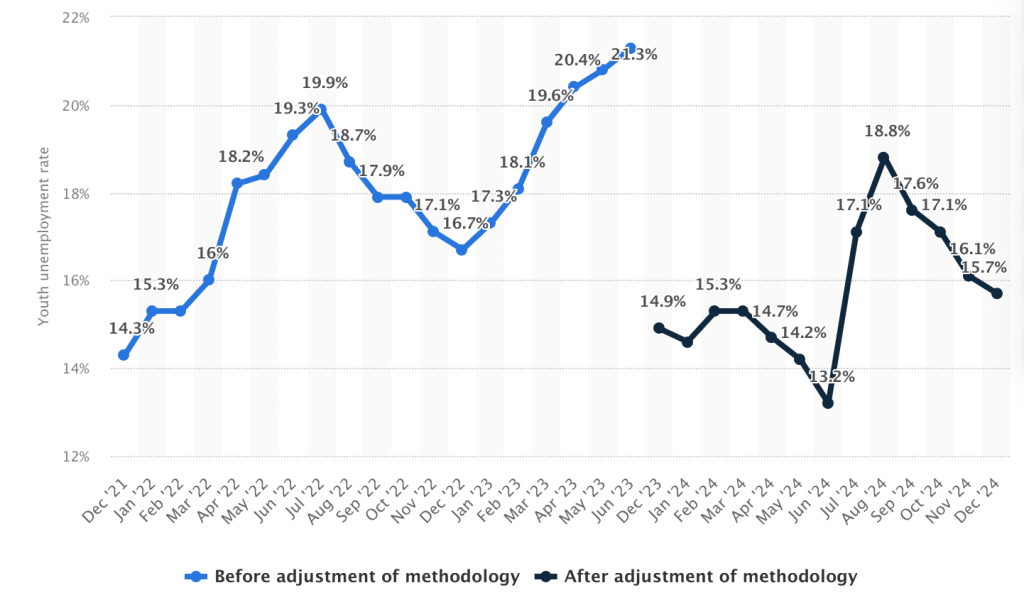

In a blog in 2021 I had mentioned China’s exorbitant artificially generated real estate bubble poses a significant risk to the Chinese economy (already called out by experts for years) which came to fruition fairly quickly in 2022. Central banks and governments’ worldwide failures to understand that high asset values vs income or when middle class continually find that they are getting squeezed each year should be at the forefront of policymakers’ problems to tackle immediately. I am trying my best to be positive but data also gives cold hard facts and the truth is world’s biggest economies all are facing extremely big economic problems. China is facing issues with significant erosion of wealth and real estate market in China has still not found its bottom. China’s unsold home inventory rose by 16% in January year on year while new homes prices fell by 5%. New launches dipped significantly in 2024 with a drop of 23%. In latest inflation reading, China reported deflation of 0.7% on a year on year basis in February’s CPI reading. Significant overcapacity in almost all sectors with wealth erosion is becoming a deadly cocktail for the economy and its consumers. This is also leading to exports as China is becoming over reliant on overseas market to tackle a domestic economy which is not showing any recovery. Deflation, declining currency and overcapacity all are making Chinese goods even more cheaper thus making them even more competitive. China has a significant incentive to dump and world may find it tough to compete if trade barriers are not erected. Chemicals, steel, auto and other sectors are reporting these issues in their earnings calls also. For context, according to New York Times, China’s auto industry has the ability to manufacture 40 million internal combustion cars a year as of end of 2024 while Goldman Sachs believes China has touched a capacity of 20 million EVs. China’s EV sector will see another capacity addition of close to 4-5 million cars this year. India’s entire domestic passenger vehicle market’s size is 4 million vehicles. United States entire sales for passenger vehicles is only 16-17 million vehicles in best of years. If world removes trade barriers imagine the deflationary trend auto sector will experience. China’s youth unemployment is high and has remained a persistent problem since 2018. China stopped reporting this data and then again came back with a new methodology to report the numbers which paint a better picture but why should that data be trusted anymore? As per latest figure, youth unemployment was down to 15% from a high of 21.3%. Answer for China remains pretty straightforward, boost fiscal spending, revive real estate market, cut overcapacity by closing down highly polluting plants and take up the slack at central government level to prevent a repeat of Japan’s lost decades.

The fallacy plaguing United States

United States is faring better than most of the world. It has outperformed Europe, China and Asia dramatically. It continued to show exceptionalism which was noticed by investors as well. S&P 500 rose by 25% each in 2024 and in 2023. With Donald Trump’s election, big long term issues facing United States are now in front and leading world into high uncertainty. United States has seen rise of far right politicians who usually call for extreme measures to tackle political climate which can bring dramatic change in world order. The rise of far right can also be traced to rising costs of healthcare, education and housing in United States.

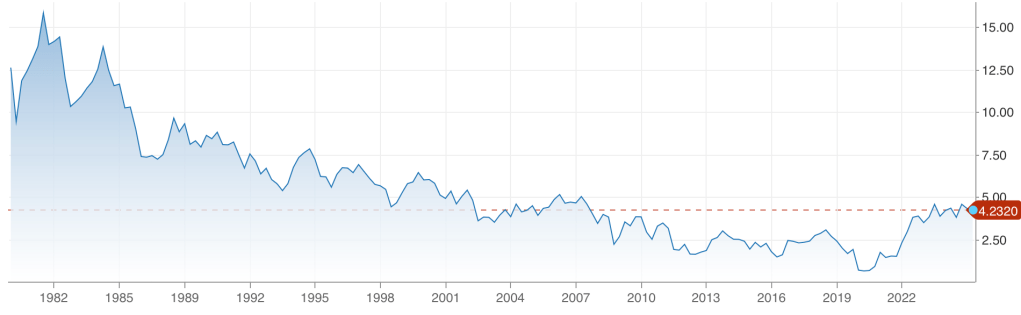

Americans are facing low income, high uncertainty, high costs and a broken job market since last few years while the rich continued to see excess growth in their wealth dramatically worsening the opinion of people about billionaires. Trump has responded to this by bringing tariffs, cutting taxes, pushing out illegal immigrants, abandoning allies, reducing its global leadership and cutting down the size of government. Problem is United States left low value manufacturing long back and being a wealthy country lot of Americans don’t prefer to work such jobs. Majority of these jobs are filled by illegal immigrants. Additionally, low cost manufacturing in United States will never win against Asia because of cost of living in US. I might as well add that Americans are living a rich life due to the existence of Asia as an extremely low cost base. Lot of this uncertainty, high inflation and market’s doubts about high level of debt at government is reflecting in financial markets. 10 year yield on US Treasuries had risen to their highest levels in the start of 2025 since 2023, touching 4.774%. Yields have also started falling quickly as recession trade is beginning to impact bond markets. Yields have fallen to 4.23% in early March. At the same time, S&P 500 has completely given up its gain since November and also is on track to reverse all gains it made since September 2024. Elon Musk and his Department of Government Efficiency might be wrong in implementation of policy of mass firings at federal level but their calls for reduction in government deficit are absolutely on point.

The asset-income equation

Asset markets and incomes at the household need to be moving in tandem. You can’t have households struggling to make ends meet and asset markets breaking new highs and making rich more rich. An economy is mostly made up of middle class which drives the majority of earnings for businesses. If middle class struggles, it is bound to impact the asset markets at some point. You can’t have an overvalued asset market while the businesses making up that market are servicing customers in middle class who are struggling in their daily lives.

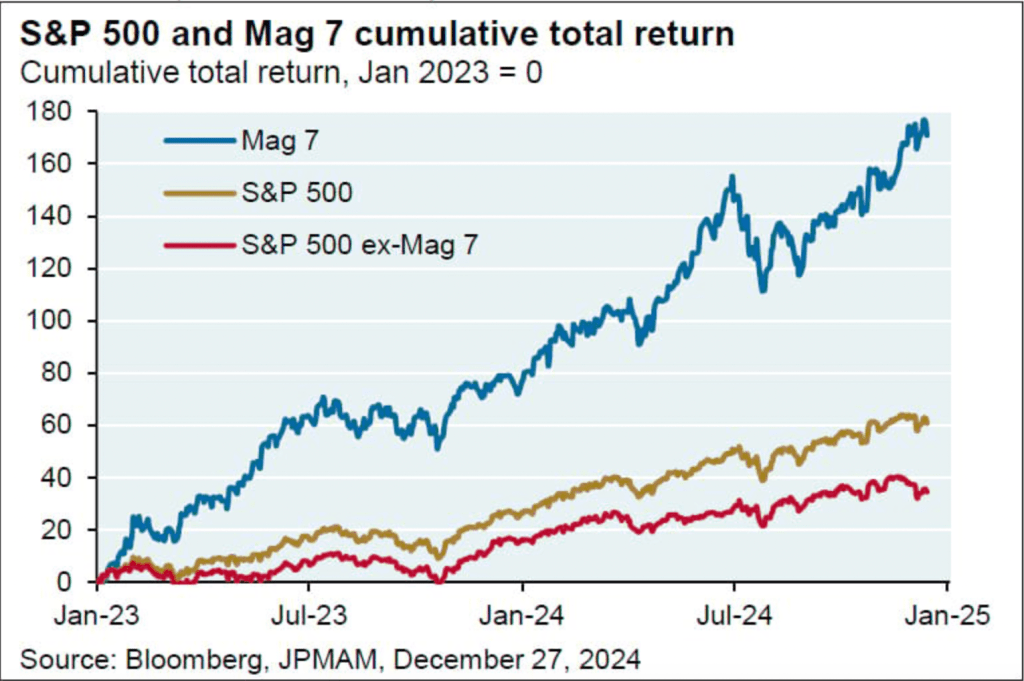

S&P 500 is facing a double whammy of increased deficit spending, high inflation and falling consumer confidence. Since Trump took office, US consumer confidence has fallen to the lowest level last seen in August 2021. At the same time, as per Reuters, S&P 500 is expected to see the best quarterly earnings season since 2021 but that is Q4FY24. The biggest driver of S&P 500, the Magnificent 7, continued to report good growth in earnings majorly driven by AI bullishness. Magnificent 7 has been the primary driver of the US equities. So for some reason if you didn’t held these stocks you would have most likely underperformed the S&P 500 index by a wide margin. These 7 stocks comprise of Apple, Alphabet, Microsoft, Amazon, Netflix, Tesla, Nvidia and Meta Platforms.

This AI led growth significantly drove S&P 500’s value in last few years. Any tapering off capex in AI or companies reducing expenditures or facing trouble monetising AI products will significantly dent the outlook for S&P 500. Part of that magnificent 7 is Tesla as well which has seen its stock pullback 50% or erosion of $850 billion plus in market value in last 2 months since Elon Musk became part of Washington. Other sectors are expected to see improvement in their earnings prospects which could lead to recomposition of S&P 500. Some sectors are struggling though. Delta Airlines just announced a cut in its earnings guidance due to weak consumer sentiment. US auto industry is under extreme pressure from Trump’s policies. With tariffs kicking in, companies may end up delaying capital expenditures and slowing the already worse job market. On ground reality vs what companies are reporting is in sharp contrast. US’ top 10% of consumers have been carrying the economy lately. They now make up close to 50% of the consumer spending in economy vs 36%, thirty years back.

An economy where things should be balanced

The point I’m trying to make is world’s two largest economies are facing asset bubbles in several pockets, high costs, low income and no job certainty. These two economies drive global markets and the economies of the rest of the world. What we might see is a slowdown over next 2-3 years or more depending on policy responses in these two economies. Economic outlook for next decade needs to be looked at with the perspective of how structural problems in these economies are going to be solved. Investing now has to be looked at from a political perspective as well. There are long term structural changes happening which could make certain assets attractive like gold, or specific stocks which may not get as influenced from these issues. Bonds could see value erosion due to high deficit incentivising US government to run high inflation but might provide hedge against short term volatility. We are entering a truly uncertain world for financial markets which might get characterised with higher volatility, rapid changes in sentiment and reordering of geopolitical world order.

-Shivang Agrawal on WordPress

Leave a comment